How to Finance a Custom Camper Van… and Why You Probably Shouldn't

Why You Shouldn't Finance Your Camper Van (And What To Do Instead)

By Vanlife Customs | The Honest Guide Nobody Else Will Write

There's a conversation we have more often than you might think. Someone reaches out, they're excited, maybe they've been dreaming about van life for years, and they want a fully built, high-end custom camper van. They've done their research, they love what we build, and then they ask: “Can I finance the whole thing?”

We could just say yes, hand them off to a lender, and move on. But that's not how we operate.

At Vanlife Customs, we build bespoke, high-end camper vans for people who are serious about the lifestyle. And because we take that seriously, we're going to be straight with you: in most cases, financing a custom camper van is not a great idea, and in some cases, it's a genuinely bad one.

This post isn't meant to scare you off. It's meant to make sure that if you do move forward, you do it with your eyes wide open. Let's talk about the real numbers, the real pitfalls, and the smartest paths forward if financing is truly the right move for you.

First, Let's Talk About Why Custom Camper Van Financing Is Complicated

Before we get into the “should you” question, it helps to understand the “why is this so hard” question.

When a bank finances a vehicle, they need to know what it's worth: not just today, but if they ever had to repossess and resell it. For a standard car or even a mass-produced RV, they use a system called NADA (National Automobile Dealers Association), which pulls from thousands of comparable sales to assign a reliable market value.

A custom camper van doesn't exist in NADA.

Every van we build at Vanlife Customs is a one-of-one. The layout, systems, materials, and craftsmanship are specific to the owner. There are no true comparables. That means most traditional banks and credit unions simply cannot write a standard RV loan for a custom build, not because of your credit, not because of the quality of the van, but because their valuation system has no frame of reference.

This creates the first domino in a chain of complications that we'll walk through below.

The Real Cost of Financing: Let's Do the Math

Before we look at specific financing options, let's establish something important: interest is expensive, and on a high-value custom build, it's very expensive.

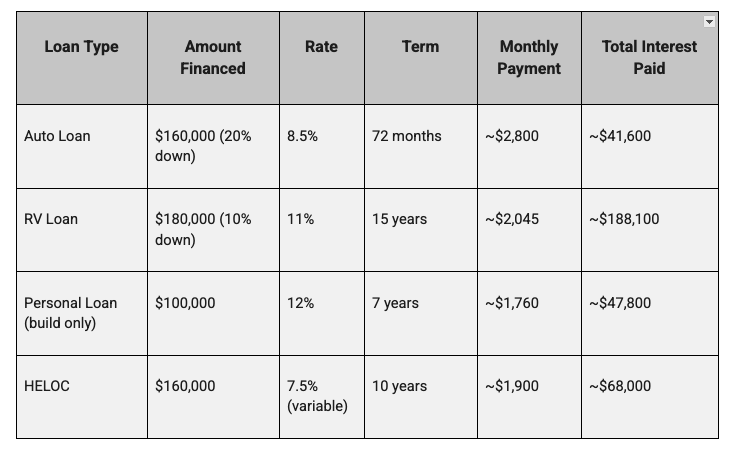

Let's use a realistic example. Say your Vanlife Customs build comes in at $200,000, a reasonable number for a well-appointed, high-end conversion. Here's what financing this project looks like across a few common scenarios:

Read those numbers again. On a 15-year RV loan, you could pay nearly as much in interest as the van itself cost. That's not a scare tactic, that's just math. Now ask yourself: does the lifestyle justify that number? For some people, genuinely, yes. But everyone deserves to see that figure before they sign anything.

The Financing Options and the Pitfalls of Each

1. Mercedes-Benz / Dealer Auto Financing (Bundled Conversion Loan)

How it works: If you're working with a Mercedes-Benz Certified Master Upfitter, it's possible to bundle some of the conversion cost into the initial vehicle loan. Special promotional rates (think 2.99% APR) are available, but only if the total financed amount stays below $80,000. For most high-end builds, that ceiling disappears before the insulation goes in.

Above $80,000, you're looking at a standard vehicle loan with APRs ranging from 4.9% to 10%, terms of 24–72 months, and a down payment requirement of roughly 50% of the upfit cost.

The pitfall: That down payment rule is a gut-check moment for a lot of people. If your van costs $60,000 and your conversion costs $120,000, you're looking at a $60,000 down payment just to get started. If you don't have that sitting in a liquid account, this path isn't available to you, and trying to force it is a recipe for financial stress.

Know before you go: Lenders also want to see relevant credit history. A 750 credit score with no prior auto financing history may actually get worse terms than a 700 score with a clean track record of comparable vehicle loans. Don't assume your credit score alone tells the whole story.

2. RV Financing Through Specialized Lenders (e.g., Umpqua Bank)

How it works: A handful of specialized lenders, Umpqua Bank being one of the most well-known, have built loan programs specifically for custom camper van builds. The process typically works in three stages: a vehicle loan to purchase the base van, a personal line of credit to fund the build, and then a refinance of both into a long-term RV loan once the van is complete.

The appeal here is real: loan terms up to 15 years, coverage of up to 90% of the total investment, and a pre-approval process that gives you confidence before you commit to a build.

The pitfall: Go back to that interest table above. A 15-year RV loan at 10–11% APR on a $200,000 van means you're paying six figures in interest over the life of the loan. You're also making payments during the build, typically 4–6 months before you ever take delivery of the finished van. And geographic restrictions apply; Umpqua's program, for example, is currently limited to Oregon, Washington, California, Idaho, and Nevada.

Know before you go: The long term feels comfortable because the monthly payment is lower. But “affordable monthly payment” and “good financial decision” are not the same thing. Stretching a depreciating asset over 15 years is a significant commitment.

3. Personal Loans (Direct-to-Consumer Lenders)

How it works: Companies like SoFi, Upstart, and LightStream offer personal loans that can be used for vehicle conversions, upfits, or large purchases without the collateral requirements of a secured loan. These can be a useful tool for financing the conversion portion of a build when the base vehicle is already owned or separately financed.

The pitfall: Personal loan rates are almost always higher than secured loans, often 10–15% or more, and terms are shorter, typically capping out around 7 years. On a $100,000 conversion, that's a significant monthly obligation at a high rate. There's also no tax advantage here, unlike some home equity options.

Know before you go: Personal loans work best as a bridge or a supplement, not as the primary financing vehicle for a six-figure build. If you're relying entirely on a personal loan to fund a high-end conversion, the math rarely works in your favor.

4. The Vehicle Loan + Personal Loan → Refinance Into RV Strategy

How it works: This is a two-step approach that some buyers use successfully. Finance the base van through a standard auto loan, take out a personal loan or line of credit to cover the conversion, and then once the van is complete and can be properly appraised as a finished RV refinance both into a single long-term RV loan.

The pitfall: This strategy requires discipline, good timing, and a lender willing to refinance a custom build (which, as we've established, isn't always easy to find). You're also carrying two separate loan obligations during the build period, which can strain cash flow. And if the refinance doesn't come together as planned, you're left managing two high-rate loans simultaneously.

Know before you go: This can work but it requires a clear plan, a trusted lending partner, and ideally a builder (like us) who can provide the detailed documentation lenders need to properly value the finished vehicle. Don't attempt this without having the refinance path confirmed before you start.

The Option We Actually Like: HELOC

If you've read this far and you're still committed to financing some or all of your build, here's the option that makes the most financial sense for the right buyer: a Home Equity Line of Credit (HELOC).

Here's why:

Rates are typically lower than any vehicle or personal loan, often in the 7–8% range, and sometimes lower depending on your equity position and the rate environment

Interest may be tax-deductible (consult your CPA. This varies based on how the funds are used)

You draw what you need, when you need it which aligns well with a phased build process

No collateral complications around custom vehicle valuation.The loan is secured by your home, not the van

The honest caveat: a HELOC is secured by your home. If something goes sideways financially, that's real exposure. This isn't a tool for someone who is stretching to afford the build, it's a tool for someone who has meaningful equity, stable income, and is using leverage strategically rather than out of necessity.

Know before you go: Many HELOCs carry variable interest rates. That 7.5% rate today could look different in three years. Factor that into your planning, and ask your lender about rate caps and conversion options.

The Honest Conversation: Who Should Finance, and Who Shouldn't

We want to be direct here, because we respect your time and ours.

Financing might make sense if:

You have 20%+ available as a down payment and aren't stretching to get there

You have strong, relevant credit history with comparable prior financing

You own a home with meaningful equity (making HELOC a viable option)

The monthly payment represents a comfortable, manageable portion of your income, not a stretch

You've run the total interest numbers and made peace with them

Financing probably isn't the right move if:

You need to finance the full purchase price with little or no money down

Your credit score is below 690, or you lack relevant financing history

The monthly payment would require significant lifestyle adjustments to manage

You're hoping the van will “hold its value” enough to justify the interest. Custom vehicles, like all vehicles, depreciate

You haven't yet saved a meaningful down payment and are looking for a way around that step

We say this not to gatekeep the dream, but because we've seen what happens when someone commits to a $250,000 build on shaky financial footing. The van becomes a source of stress instead of freedom. That's the opposite of what van life is supposed to be.

So What's the Move?

If you're not quite in a position to move forward today, here's what we'd suggest:

Set a savings target. Know your build budget, calculate 20–25% of that number, and make that your cash goal before you finance anything.

Build your credit profile. If you haven't financed a comparable vehicle before, consider doing so. Lenders want to see relevant history.

Talk to your bank about a HELOC now, even if you're 12–18 months out. Understanding your equity position and what you'd qualify for is valuable information.

Come talk to us. We're happy to have a real conversation about what a build costs, what the timeline looks like, and how to plan for it financially. We'd rather spend an hour helping you get ready than rush you into a project you're not set up to enjoy.

The dream of a custom camper van is worth doing right. At Vanlife Customs, we put everything into every build, and we want the people who drive them off our floor to feel nothing but excitement when they do.

That starts with being honest about the money.

Ready to start the conversation?

Contact Vanlife Customs and let's talk about what's possible.

Vanlife Customs builds high-end, bespoke camper vans for clients who are serious about the lifestyle. Every van is a one-of-one, built to your specifications, and held to an uncompromising standard of craftsmanship.